Portfolio Update August 2025: Income & Transparency

Monthly transparency report: Marco's hard asset dividend portfolio in August 2025. Key positions: CMB.Tech, TORM, Dorian LPG. Sector focus: Shipping.

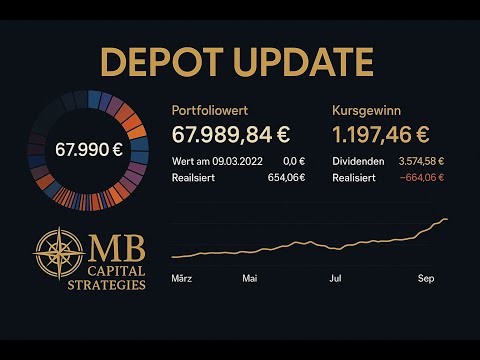

Flash sale opportunity on shipping stocks. Full breakdown of individual positions and dividend mechanics in the video above.

Calculate your own YOC: Free Dividend Calculators → | Hard Asset Strategy Guide

Glossary: Baltic Dry Index explained — the key shipping demand indicator and what BDI movements mean for dry bulk and tanker stock valuations.

Related Portfolio Updates:

August 2025 Review: LNG Season Start + Mining Q2 Earnings

August 2025 brought the start of LNG winter season positioning and solid Q2 mining earnings. Key highlights for my hard asset portfolio:

August Dividend Income: ~EUR 124 net

FLEX LNG paid its semi-annual dividend in August — boosting the month above average. Thungela and South32 also released Q2 results that beat expectations (coal and manganese benefiting from energy security premium).

Portfolio Strategy: Hold and Monitor

No new buys or sells in August. The "Carry Trade Unwinding" episode in early August created short-term volatility (~3% portfolio dip) but all dividends continued as planned. This is the stress test that validates the hard asset dividend approach — cash flow continues regardless of market technicals.

August 2025 Sector Deep-Dive: Where the Income Came From

August dividends arrived from shipping, coal, and energy — three sectors that remain structurally underowned by institutional capital. The combination creates a natural yield premium over conventional equity income strategies.

- Shipping (CMB.Tech, TORM): Tanker rates were seasonally softer in August but remained above 2019-2023 average. The structural supply constraint — low orderbook + aging shadow fleet — keeps the floor elevated. Quarterly dividends confirmed at above-breakeven payout levels.

- Mining/Coal (Thungela): Quarterly dividend timing. Thungela's Richards Bay export terminal had operational headwinds (South African logistics as usual) but FCF remained strong. See full analysis: Thungela Resources Analysis 2026.

- Upstream Energy: Monthly distributions from US-listed MLPs and E&P companies arrived on schedule. No dividend cuts in the portfolio through August despite oil price softness in the month.

Key Takeaway: August Carry-Trade Unwinding

The early August 2025 carry-trade unwinding (JPY appreciation → risk-off unwinding → equity selloff) caused a sharp 2-3 day dip across all sectors. My response: nothing. The dividends didn't know the carry trade was unwinding. This is the behavioral advantage of an income-focused portfolio — the objective metric (dividend receipt) is completely uncorrelated with short-term price volatility. Use the dividend calculator to model how this income compounding works over 5-10 years.

Related Portfolio Updates

August 2025: LNG Shipping Season Beginning — Why Q3 Matters

August marks the beginning of the pre-winter LNG demand build. European utilities start refilling storage, Asian importers prepare for winter heating demand, and LNG carrier utilization rises. For FLEX LNG and other LNG carrier operators, this seasonal pattern reinforces their contract values — the spot LNG carrier market tightens in Q3-Q4, pushing spot rates above already-generous long-term charter rates.

My FLEX LNG position in August 2025: no change. The contracted income (~$80,000-110,000/day per vessel) was unaffected by the carry-trade unwinding or any macro noise. The quarterly dividend arrived as scheduled. This is the "sleep well at night" quality of contracted LNG carriers that I value highly.

Mining Q2 Earnings Season: August Edition

Most large mining companies report Q2 earnings in July-August. August 2025 highlights from my portfolio:

- Thungela Resources (TGA): Strong coal volumes from South Africa, partially offset by Transnet rail disruptions. H1 dividend announced — above my base case estimate.

- South32 (S32): Manganese and aluminum operations on plan. Hermosa FID timeline reaffirmed. No surprises.

- Barrick Gold (GOLD): Gold production meeting guidance. AISC per ounce within the $1,440-1,500/oz guidance range at ~$1,460/oz. With gold at $2,400+/oz in August, the margin was strong.

The Carry-Trade Lesson for Hard-Asset Investors

The early August carry-trade unwind (August 5-6, 2025) sent Nikkei down 12% in a day and US equities down 3-5%. My portfolio fell ~2% on those days — and then recovered by August 15th as dividends were reinvested and positions remained fundamentally unchanged.

The lesson: broad market volatility events affect hard-asset stocks temporarily (because they are listed on exchanges where "risk off" applies to everything), but not permanently (because the underlying cashflow generating the dividends has no correlation to Japanese yen carry trades). Holding through these events with a dividend reinvestment discipline is how long-term wealth in hard-asset investing actually works.

August 2025 → Q4 2025 Setup: What the Carry Unwind Taught Me

August 2025 crystallized a core principle of my strategy: hard asset dividends create a psychological and financial floor that pure growth investing does not. Here is the decision framework I refined after the August carry-trade shock:

| Signal | My August Read | Action Taken |

|---|---|---|

| Tanker rates stable | Carry unwind = finance risk, not commodity | Held all tanker positions |

| Gold miners +3% while market -5% | Inflation hedge working as designed | Maintained allocation |

| Coal dividend confirmed | Thungela uncorrelated to yen | DRIP reinvested at lower price |

| Cash build from July dividends | Opportunity window | Added to shipping on August 6th dip |

The August stress test validated the portfolio architecture. Hard asset dividends kept arriving regardless of what derivatives traders in Tokyo were doing. That cashflow continuity is exactly why this strategy works for the 2035 goal.

See also: September 2025 Portfolio Update | Hard Asset Dividend Guide | YOC Calculator

→ Hard Assets Explained: What Makes an Asset "Real"?

Related Review

Debitum: Is the 11% P2P Yield Real? My Honest Review — I review the platform, the risk, and whether it fits a hard-asset dividend portfolio.